All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication.

Valmas Associates services include Greek Real Estate Law, Property Construction & Acquisitions, Property Management services and Golden Visa permanent residency applications. Contact us for our rates & services. The Greek Golden Visa Law (permanent residency by real estate investment e.g. via acquisition of property in Greece) has been amended. The minimum investment threshold on purchases of property to the end of receiving a Greek permanent residency permit (renewable every five years) has changed in several areas of Greece. More specifically, the minimum investment threshold has increased on several areas, whereas the number of properties to be acquired has been limited to one in these areas. The core changes to the above can be summarised as follows: 1. Purchases of real estate in the central, north and south section of Athens as well as in Thessaloniki, Mykonos and Santorini are subject to the amendments in the law namely: a. Investment threshold is established at 500,000 EUR and b. Investment should be in one property only. 2. Purchases of real estate in the rest of Athens’ eastern and western suburbs as well as the remainder of Greece, will be falling under the thresholds of 250,000 EUR, whereas the threshold amount (250,000 EUR) could be met by purchasing one or more properties i.e. there are no restrictions as in the areas described under 1. above. Taking advantage of the current legal regime It is also specified that, had investors required to take advantage of the current legal regime, where thresholds are at 250,000 EUR all over Greece (including Mykonos, Santorini, Athens centre etc.) with no limitations to one property, they should transfer 10% of the transactional value to the sellers by the 30th of April 2023 (through a private or notarial agreement) whereas the final conveyancing agreement and respective bank transfers of the remainder of the agreed sum, should take place by (no later than) the 31st of December 2023. So for example, an investment in two properties in the centre of Athens valued at 150,000 EUR each, will still be possible as long as a. a deposit of 10% is paid to the sellers by April, 30th 2023 (extended until July 31st, 2023) and b. the final conveyancing agreement is signed by the 31st of December 2023.

0 Comments

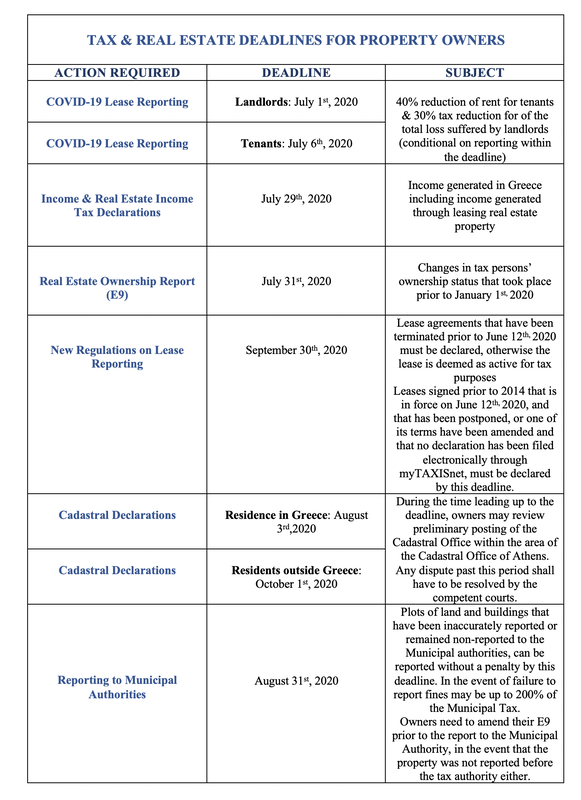

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication. The following form the upcoming deadlines for real estate owners and tenants of properties for the remainder of 2020.   All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication.

In this newsletter we deal with the implications for GDPR following the outbreak of COVID-19 in relation to: a. employers when balancing between confidentiality of infected individuals (employees) and public interest (informing others who have been put at risk); b. employees while working remotely. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication.

Article 285 of the Greek Penal Code contains a provision termed Violation of measures to prevent epidemics. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication.

In this newsletter we outline the stages of a real estate transaction in Greece. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication.

On the 25th of February, the Greek Government passed (and published on the Government Gazette) a Legislative Act termed "Urgent Measures for Avoidance and Restriction of Spreading Coronavirus (COVID-19)". The measures contained in the 5 Articles of the Legislative Act may be imposed and had they come into effect, they should further be defined by Ministerial Decisions of the competent Ministries. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication.

This article examines the possible implications and viability of claiming force majeure in the light of disruptions to global trade that the recent COVID-19 outbreak has caused.  All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication.

EU countries lost €137 billion in Value-Added Tax (VAT) revenues in 2017 according to a study released by the European Commission in September 2019. The loss in VAT revenue has prompted some critical actions by the European Commission and initiated some changes to the EU VAT rules and accounting processes. The major changes, under EU VAT legislation, do not take effect until 2022 or later, but there are some immediate steps that the EU implemented that took effect on Jan. 1, 2020. These are referred to collectively as the Quick Fixes, and will impact businesses engaged in cross border trade involving the movement of goods. There are four Quick Fixes that have taken effect and as of Jan. 1, 2020 businesses should have been taking action accordingly, so that they remain in compliance.  All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication. LAW 4646/2019: REFORMS IN REGARD TO THE HELLENIC INCOME TAX CODE Article 2: Alternative taxing to income received abroad for natural persons (HNWIs) that move their tax residence to Greece A taxpayer who moves her/his tax residence to Greece can be subjected to an alternative method of taxation for income received abroad if both of the following conditions are met:

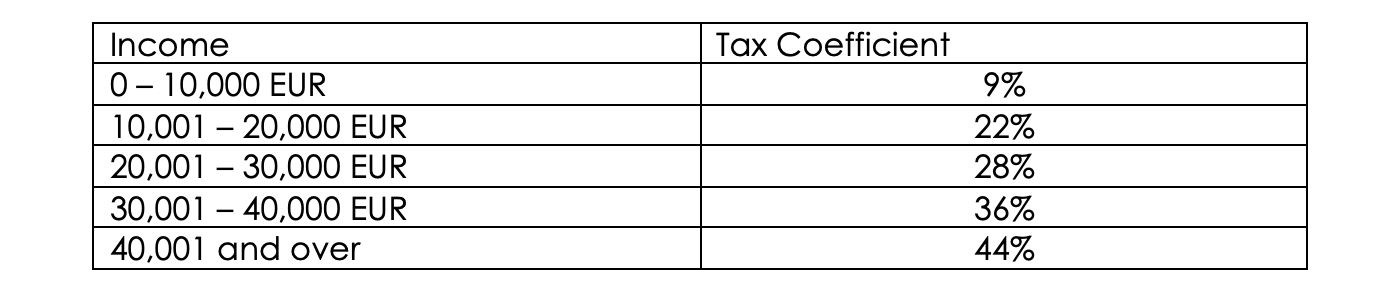

Had the application been accepted, the person shall pay a fixed tax of 100,000 EUR per year regardless of the income generated abroad. This person has an option to request the extension of the above provision to relatives. In that case an amount equal to 20,000 EUR per relative should be paid per year. Assets located outside Greece are exempt from the Greek inheritance or gift tax. The funds imported in Greece are not required to be justified. Income generated abroad is not reported. The maximum duration of the program is 15 years. Application procedure outline: • Filing of an application by 31 March of the relevant tax year; • Approval of the application by the Greek tax authorities within 2 months from filing; • Notification of the foreign tax authorities regarding the transfer of the applicant’s tax residence in Greece; • Payment of the annual tax within 30 days from the date of the application approval. Article 6: Amendment of Article 15 of the Income Tax Code in regard to tax rates for wages, pensions, business activity of persons.  Example: A worker declares income of 12,000 EUR per year. He/she will be taxed with 9% for the amount of 10,000 EUR and 22% for the remaining 2,000 EUR. Article 11: Corporate Social Responsibility (CSR) Deductible Expenses Expenses related to CSR activities are now classified as expenses made in the interest of the company and within its ordinary course of business. CSR expenses are tax deductible under the condition that the company has accounting profits in the tax year in which the expenses are made. Article 12: Deductions Related to Employees and the Protection of the Environment 130% deduction has been enacted for expenses made from 01/01/2020 onward, for the following expenses made for: · purchase of monthly or annual season tickets for public transportation; · leasing of company cars of zero or low emission up to 50gCO2/Km, with Retail Price Before Taxes (RPBT) up to 40,000 EUR; · purchase, installation and operation of publicly accessible charging points for electric vehicles of zero or low emission up to 50gCO2/Km. Article 16: Deduction of tax for service-related expenses made toward the energy related, operational and aesthetic upgrade of buildings. 40% of the expenses incurred from services performed within the context of the energy, functional/operational and aesthetic upgrade of buildings will reduce individuals’ income tax and shall be distributed in four equal parts for the four following years. The maximum amount of deductible expenses can be 16,000 EUR. The above tax rebate is granted to private individuals subject to special requirements and shall apply for expenses (services only) incurred during calendar years 2020-2022. Such expenses must be paid by electronic means of payment. Article 22: Reduction of Corporate Income Tax (CIT) The nominal corporate income tax (CIT) rate is reduced to 24% (formerly 28%) for fiscal years 2019 onward. Article 24: Reduction of Dividend Withholding Tax Dividend withholding tax is reduced to 5% (formerly 10%) as of 01/01/2020. Article 26: Corporate Income Tax Prepayment CIT prepayment which was assessed upon the filing of the CIT return for fiscal year 2018 is reduced to 95% (formerly 100%). Article 28: Betterment Tax for Sellers Further Suspension Betterment Tax for Sellers: Pursuant to Article 41 of Law 4172/2013, a betterment tax on the transfer of real estate, will be imposed on the seller of real estate property in Greece with a coefficient of 15 percent calculated upon the profit the seller made by the sale of the property when compared to the original purchase value of the property. There are reduction factors limiting the amount of tax a seller will be called to pay upon the profits from the resale of his/her property based on amount of time they kept ownership and other factors. In the event a property has not been purchased and e.g. has been inherited or gifted, then the acquisition price will be based on the tax originally paid when one inherited or was gifted the property. The betterment tax has been further postponed until the 31st of December 2022. Article 29: Digital platforms (e.g. Airbnb) obligations to disclose information to the Hellenic Independent Authority of Public Revenues (ΑΑΔΕ). Disclosure obligations are introduced for administrators of any digital platform active in the sharing economy, within specified deadlines and with penalties provided for non-compliance for both the platform and third parties involved (Network Service Providers and users of the platform for the provision of services). Maximum penalties come up to 100,000 EUR for non-compliance of Network Service Providers and to 5,000 EUR to “sellers” on the above platforms, to the requests of the Hellenic Independent Authority of Public Revenues (ΑΑΔΕ). Article 39: Amendment of the VAT Code in regard to Suspension of VAT on Property Transfers. For the period 2020-2022, the sale of properties by constructors/developers of buildings (that would normally be subject to 24% VAT) will be exempt from VAT. Following an application of a property developer/construction company offering properties for sale, there is a compulsory suspension of VAT until 31/12/2022. The suspension will be applied to the total number of unsold properties of the developer. The application should be filed no later than 6 months from the coming into effect of Law 4646/2019 (for already issued permits) whereas for new building permits the application should be filed within 6 months of the issuing of the building permit. Thus, the exemption covers both buildings which have been completed (built) with building permits following 01/01/2006, as well as those that will be built within the aforementioned three-year period. Article 51: Amendments in respect to tax values of zones and properties In order to determine the tax values of properties that are transferred for any reason (sale, parental gift etc.) prices will now be affected by coefficients such as construction quality, age, position on the building block, floor, location on a central spot or lack thereof, tourist value in respect to agricultural plots etc. New committees will be assigned this task.   All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication. The below newsletter is an interpretation & analysis of the announcements made by Greece's Prime Minister in relation to - among others - reforms on property transfer taxes & construction activities in Greece. These were made during a gala event organized by The Economist in Athens Greece on October 23rd. 2019 CURRENT PROPERTY TRANSFER TAX REGIME: Pursuant to current Greek tax law, a 24% VAT is imposed on the first acquisition of apartments and properties for which the building permit was issued after the 1st of January 2006. All other properties are exempt from VAT and a 3.09% property transfer tax is imposed on the buyer. PROPOSED BILL'S PARTICULARS: 1. The Greek Government plans to pass a new law soon, suspending VAT for 3 years on unsold brand new properties from developers for which the building permit was issued after January 1st 2006 and - at least - until the lapse of the 3 year suspension. 2. In an effort to further boost the real estate market in Greece, the government shall further suspend VAT on properties not yet completed for which building permits where acquired from 1/1/2006 as well as on newly or to-be-acquired building permits within this period of suspension. This way, the government aims to jump-start building activities. The details of the above bill have not been fully disclosed yet. 3. According to the announcement from the Prime Minister (during The Economist's gala event), the suspension of VAT shall also affect property owners who acquired apartments under the antiparochi (αντιπαροχή) system. Antiparochi (αντιπαροχή) is a sui generis Greek arrangement, whereby the owner of a plot of property is compensated with apartments in lieu of payment for the land that he relinquished to the developer who built an apartment block on the plot. We will keep you posted when the final bill has been implemented in national legislation. HOW WILL BRAND NEW PROPERTIES BE TAXED IF VAT IS SUSPENDED: The most probable scenario is that sales of the above properties will be taxed with 3,09% property transfer tax, (that is imposed on buyers of second hand properties) instead of the current 24%. EXAMPLE: In practice if a buyer acquired a brand new apartment at 200,000 EUR today, he/she would be called upon to pay 48,000 EUR on VAT. When the new law comes into effect, in most circumstances, they will be called upon to pay just a little over 6,000 EUR for a property purchase value of 200,000 EUR which is what second hand property buyers pay. The saving in the above example is 42,000 EUR. OTHER ANNOUNCEMENTS: Betterment Tax for Sellers Pursuant to Article 41 of Law 4172/2013, a betterment tax on the transfer of real estate, will be imposed on the seller of real estate property in Greece with a coefficient of 15 percent calculated upon the profit the seller made by the sale of the property when compared to the original purchase value of the property. This law's coming into force is going to be suspended for a further 3 years. The government has also announced that it will examine the abolition or amendment of this law at the lapse of the suspension period. Deduction of Income Tax for Works/Renovations Carried out on Properties towards their Aesthetic & Environmental Upgrade This is a proposed law that is still being debated.   All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication.

The following constitute some mere keypoints from Newsletter E.2141 ΑΑΔΕ 16/07/2019 which provides extensive information on tax matters related to income from short-term leases:

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication.

The new Greek government is due to pass a draft bill by mid-August 2019, aiming at further increasing the potential for growth of the Hellenic Economy with some measures targeting at strengthening real estate ownership and development of real estate properties, as well as reducing taxation and creating a more solid, stable and tax friendly environment for private & business persons and companies. Priorities of the Hellenic Ministry of Finance on the forthcoming Bill due in August 2019 include: · Decrease of tax rate in businesses from 28% to 20% within the next two years. In 2020 income tax will drop to 24% whereas in 2021 it will further drop to 20%. · Decrease of dividents’ tax from 10% to 5% in 2020. · Decrease and universal reduction on the uniform property ownership tax (ENFIA) by 30% within the next 2 years. · Tax reduction equal to 40-50% of the expenditure for the energy related, operational or aesthetic upgrade of buildings. · Further suspension of the Betterment Tax for Sellers (tax on the profits from the sale of immovable property) for an additional term of 3 years and a revision of the law 4172/2013 with a view to being drafted a new basis after the fourth year (2023 or 2024). · Suspension of VAT tax on real estate developers/building activities (affecting sales of newly developed properties). · Enactment of an introductory tax coefficient on private persons from 22% today to 9% for income up to 10,000 EUR annually, without a reduction on the non-taxable income coefficient and the creation of a progressive tax scale with lower tax rates up to the highest incomes. Also, a gradual abolishment of the solidarity levy is being discussed. · Decrease of VAT rates from 13% to 11% and from 24% to 22% within the next 4 years. · Progress on the staffing of the Independent Authority of Public Revenues (AADE) with 12,500 employees. · Fully digitized and electronic processes/services from the Independent Authority of Public Revenues (AADE).  All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication.

The following article published in our third newsletter provides a simple guide on the declaration of your rights with the Hellenic Cadastre with links to the Hellenic Cadastre's website. Abstract The Hellenic Ministry of Environment and Energy and the Hellenic Cadastre have initiated the process of cadastral surveys. These projects cover the remaining 42.4% of the country's rights, which is about 16.5 million rights, corresponding to 63.4% of the territory of the State that has not been surveyed yet in order to facilitate town planning and effective protection of property rights. During this process the beneficiaries of property rights located in such regions must declare these rights before the competent Cadastral survey offices, pursuant to Law 2308/1995, under specific deadlines (and possible extentions) announced at www.ktimatologio.gr. The government's target is to have the entire territory of Greece registered with the Hellenic Cadastre by 2022. The below article provides a very basic guide. For more information visit http://www.ktimatologio.gr Regions under survey and communicating with the Hellenic Cadastre Please visit: http://www.ktimatologio.gr/sites/en/cadastralsurvey/Pages/kuUtbigTQbkVTDd_EN.aspx in order to find out if your property is under survey. Expatriates can also communicate directly with the Hellenic Cadastre at the following link: http://www.ktimatologio.gr/sites/en/Pages/ContactRegistration.aspx Rights to be declared All rights that are mandatory to declare pursuant to the provisions of the Hellenic Civil Code must also be declared with the Hellenic Cadstre i.e. full ownership, bare ownership, usufructs, mortgages, prenotations of mortgages, easements, property assurances, seizures, lawsuits, registrable long term leases, time sharing contracts. Remember to:

STEPS 1. To Participate Submit a Declaration of Ownership before the deadline Check the outcome of the cadastral survey during the preliminary public presentation and the public presentation of the cadastral data Submit a review request during the preliminary public presentation (if errors are detected) Submit a correction or objection application during the public presentation (if errors are detected) 2. How to Declare - What you need to gather Declaration form and photocopies of:

3. Locate Your Property Through the Ortho-image View Application 4. Attach A topographic diagram is necessary if one of the following circumstances are met:

5. Pay the fee 35 EUR per property right, 20 EUR for auxilliary spaces and no more than 70 EUR for 2 or more agricultural parcels in the same Local Authority. 6. Submit

Deadlines Τhe deadlines to proceed to the filing of above declarations vary for each area while extended deadlines apply for residents abroad. All relevant deadlines can be found at http://www.ktimatologio.gr/sites/en/Pages/Default.aspx.  The following article published in our second newsletter provides an insight on some key legislative developments regulating short-term leases/rental of property. It may be of interest to property owners leasing via Airbnb and other digital platforms. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication. 1. Law 4472/2017 Law 4472/2017, published in the Government Gazette on May 2017, introduced provisions regulating short- term leases via digital platforms. It also granted powers to the Ministers of Economy and Tourism to set limitations, had this been deemed as necessary, to specific geographical areas and for reasons of protecting ordinary tenancies/leases. Such limitations refer to the number of properties per person and on the number of days the property can be leased per calendar year. Authorization has also been granted to the Governor of Independent Public Revenue Authority (AADE) to determine the procedural technicalities in connection to the operation of the Short Term Leases Register and the Short Term Leases Platform. 2. Decision 1187-2017/11/23 Decision 1187-2017/11/23 of the Governor of the Independent Public Revenue Authority is the first decision that applies to cases of income earned as of January 1st 2017 while the procedural technicalities set by the Governor’s decision have come into effect from January 1st 2018 onward. The Decision has clarified issues and questions that had arisen following the enactment of Law 4472/2017. 3. Clarifications in the light of Law 4472/2017 and Decision 1187-2017/11/23 a. Properties falling within the scope of Law 4472/2017 & Maximum Duration of short-term leases As property is defined the apartment, detached house, (with the exception of detached houses which have been characterized as such by the annulment of the establishment of horizontal property) any other form of dwelling with structural and functional autonomy, rooms within apartments or detached houses. A further clarification is that the property may be (i) a single space or (ii) leased in parts. Duration shall be up to one year. b. Property Manager As manager of a short-term lease property is defined, any natural or legal person or any legal entity that undertakes the process of posting a property on digital platforms for the purpose of short-term leasing; and generally the one that makes any arrangements for the short-term leasing of the property. The property manager may be either the owner of the property or a possessor or a holder of the usufruct right or a sub-tenant or a third party representing the owners by virtue of special legal arrangements (parent of minor, bankruptcy trustee, will executor etc). In essence, the property manager is obliged to comply with the obligations set out by this special regime of short-term leases vis-a-vis the tax authorities. Only one property manager is allowed per property. Therefore, in cases of joint-ownership of a property, only one of the joint owners shall act as the property manager. c. Beneficiary of short-term lease income It can be an individual/private person or legal entity. The Property Manager and co-owners of a jointly owned property are taxed as income beneficiaries. Exceptionally, when the Property Manager is a third party, as defined above, she/he is not the income beneficiary. d. Property Owner The property owner is in most cases both the property manager and income beneficiary. However, it is not always so. For example, in the case where the owner of a property has leased the property and allows sub-letting to his/her tenant, the sub-lessor will act as property manager and income beneficiary. The owner of the property should thus merely report/declare the long term lease between himself/herself and the sub-lessor to the standard Electronic Platform of AADE for declaring/reporting real estate leases. Then the sub-lessor shall subsequently undertake his duties as property manager and post the make the necessary declarations. e. General conditions for the short-term lease of property through digital platforms (i) the property manager must be registered in the “Short Term Residence Property Registry” of the Independent Authority for Public Revenue (AADE), unless he/she possesses an Authorized License. This registration must have been made separately for each leased property by entering the data (beneficiaries of income, share of ownership etc.) necessary for the determination of the annual income per beneficiary; (ii) the registration number in the above Registry must accompany the posting of the property on digital platforms, at a clearly visible space, as well as in every marketing action and material. In the event the property manager is under an Authorized License, the display of the number of the Authorized License is sufficient. f. Procedure of submitting short-term leases The procedure is effectuated online at the homepage of www.aade.gr by the Property Manager, using his/her personal TAXISnet credentials. g. Minimum necessary content of the short-term lease statement The minimum necessary short-term lease particulars are the following: a) the registration number in the Short Term Residence Property Registry, b) the total lease fee agreed or the total amount under the annulment policy, c) the name of the digital platform through which the lease was concluded, d) the particulars of the lessee, e) the commencement and expiration date of the lease, f) the method of payment of the lease fee. h. Deadlines for submitting short-term leases The declarations of short-term leases shall be filed by the 20th of the month following the departure date of the lessee from the property. Amendments can be made by the 28th of February of the year income tax declarations are due and before the finalizing of the Register for Short-Term Leases. 4. Obligations for Property Owners Property owners or usufructuaries who delegate the management of the property within the context of the short-term leases to third party property managers need a. to file a declaration of lease data with the platform, maintained by the Ministry of Finance and b. to declare the identity of the Property Manager. The above declaration precedes the registration of the property with the Short-Term Leases Registry for short-term lease properties. Failure to do so results in them being deemed as Property Managers by the tax authorities. In the event of multiple owners, where one is the property manager, the other co-owners are not required to file a declaration of lease data. 5. Obligations for Property Managers The main obligations for property managers are the following: (i) Property managers list the property for lease on digital platforms. As aforementioned, the registration number of the property with the Short-Term Leases Registry must be included in the listing with the digital platforms and any advertisements. (ii) Property managers shall report all the necessary information for the calculation of the annual revenue per income beneficiary. The Short-Term Leases Registry is finalized each year before the beginning of the period of filing of the annual income tax returns for individuals. Had the necessary data for the calculation of the taxable income per income beneficiary not been filled by such date, so that 100% of the income is taxed, the income percentage that has not been attributed to an income beneficiary is taxed in the name of the property manager, unless he/she has deposited the corresponding amount with the Consignments and Loans Fund (he/she is obliged to deposit with the fund income attributable to unknown income beneficiaries). (iii) Property Managers need to report a. properties no longer been offered for short-term leases and b. themselves ceasing to act as property managers. In case any of the above violations is assessed by the authority, the property manager must comply with the requirements set out by law within 15 days. In case the same infringement occurs within a year from the date the relevant penalty is imposed, the penalty is doubled. Had the same infringement occurred again, the penalty is quadrupled. 6. Penalties A penalty of 5,000 EUR is imposed on property managers who: (i) Fail to register with the registry; (ii) Fail to indicate the registration number or special mark (where applicable) on digital platforms or through ads on the media. A penalty equal to double the lease amount is imposed in case a non-accurate declaration of short term lease is made. A penalty of 100 EUR is imposed in the event of a late declaration of a short-term lease.   All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication.

Our first newsletter examining some recent key developments on tax law affecting individuals owning real estate and businesses in Greece is out and available for download.  Greece’s special residence program for foreign investors has taken off, reflecting increasingly bright growth prospects as the country emerges from economic crisis and its growing importance as a gateway to the European Union. In the last year, the number of foreigners awarded a Greek Golden Visa has soared: rising by more than 40% from a year earlier.

Launched five years ago at the height of the country’s economic crisis, the Golden Visa program is now coming of age amid a new wave of investor interest, particularly from countries like China, Russia and Turkey. The reasons are several: from Greece’s sunny Mediterranean climate and high quality of life, to its low property prices. A budding economic recovery plays a role for some investors, for others its political uncertainty abroad. And since the law was revised in 2015, Greece’s Golden Visa has become still more attractive to foreign investors, comparing favorably with similar programs in countries like Cyprus or Portugal. A stepped up promotion program - in the last two years Enterprise Greece has showcased the program at trade fairs from Moscow to Beijing to Constantinople – has also helped. Greece’s Golden Visa program grants a permanent residence permit – and access to 26 Schengen area countries - to individuals and their families who invest a minimum of €250,000 in Greece, such as in real estate or other productive investment. According to the latest data from end November, a total of 2,170 Golden Visas have been issued directly to foreign investors – and more than 5,000 including family members - up from 1,522 at the end of 2016. After falling by as much as 50% from their pre-crisis peak, and with booming summer tourism buoying short-term rentals, Greek property prices now offer a highly attractive yield on investment, say industry experts. That has drawn investors from China, who now account for almost half of Golden Visa holders. But another reason is Greece’s political stability and EU membership. In the past year, nationals from several neighboring Mediterranean countries – most notably Turkey – have also been buying up Greek real estate, lured both by the access to the EU that a Golden Visa offers, as well as to diversify their holdings away from an uncertain climate in their home country. Source: Enterprise Greece Valmas Associates have been acknowledged as one of the leading professionals in the particular field. We have represented and/or we are currently representing clients from Africa, the Middle-East, Asia & America in the field of the Residence Permit by Property Investment in Greece (Golden Visa). You may contact us on the relevant section of our website so that we further assist you. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication.

It has come to our attention that some individuals of unknown identity have been using masked/spoof emails appearing to be generated from our law firm. If you receive a suspicious email referencing Valmas Associates or appearing to be from our law firm (e.g. from a "spoofed" Valmas Associates email address using our website name extension athenslawoffice.com) we suggest the following:

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without prior permission of the publisher. Application for permission for other use of copyright material including permission to reproduce extracts in other published works shall be made to the publisher. Full acknowledgment of author, publisher and source must be given. Nothing in this newsletter shall be construed as legal advice. Professional advice should therefore be sought before any action is undertaken based on this publication. Golden VISA Program in Greece and buying property in Greece or buying a house in Greece have now been made easy. Visit the relevant pages in our website and get information or contact one of our Greek Lawyers for more info. |